Trump tariffs: effects on the market

Donald Trump’s trade policy, a cornerstone of his economic vision in his first term (2017–2021) and now his second (started January 2025), has escalated with sweeping tariffs aimed at protecting U.S. industries, narrowing the $947 billion 2024 trade deficit, and boosting domestic manufacturing. Trump has placed a 90 day pause on his tariff which started on April 9, 2025, this which has market volatility, sparked global retaliation, and strained supply chains. This high-stakes gamble tests Trump’s promise of economic sovereignty against the risks of inflation and trade wars, with markets caught in the crossfire. Here’s an updated analysis of the mechanisms, numbers, and market dynamics, enriched with critical commentary.

The Tariff Plan: What’s on the Table?

Trump’s 2025 tariffs dwarf his first-term measures. In 2018, he imposed 25% tariffs on $50 billion of Chinese goods, 10% on $200 billion more, and global levies of 25% on steel and 10% on aluminum. Now, the April 2 “Liberation Day” plan set a 10% baseline on all $3 trillion of U.S. imports, with up to 145% on China’s $600 billion in goods (2024 figures). Canada and Mexico faced 25% tariffs on $400 billion and $300 billion, respectively, under the USMCA ($2.6 trillion trilateral trade). On April 9, Trump paused most tariffs for 90 days, keeping 10% on most nations but raising tariffs on China to 125% and again to 245%, with smartphones and electronics exempted. The White House projects 500,000 manufacturing jobs by 2030, but critics highlight supply chain inertia. Over 70 countries are negotiating trade deals to avoid tariffs, per U.S. Trade Representative Jamieson Greer.

This aggressive stance reflects Trump’s belief that tariffs are a blunt but effective tool to force concessions, yet the scale risks alienating allies like Canada, potentially fracturing the USMCA. The China exemption for electronics suggests pragmatic concessions to consumer demand, but the 125% tariff signals unrelenting pressure on Beijing, which could backfire if retaliation escalates. The 90-day pause buys time but underscores the policy’s volatility, leaving markets and negotiators in limbo.

Immediate Market Reactions

Markets have been going crazy. In March, the S&P 500 fell 2.3% (120 points), and the Dow dropped 1,100 points (2.5%) all on tariff fears. By April 7, the S&P 500 neared a bear market, down 18.9% from February’s peak, with a 4.7% plunge. The April 9 pause sparked a historic rally: the S&P 500 soared 9.5% (474 points) to 5,456.90, the Dow surged 2,963 points (7.9%) to 40,608.45, and the Nasdaq jumped 12.2% to 17,124.97—the S&P’s biggest gain since 2008. April 10 saw a pullback, with the S&P 500 down 3.46% and the Dow off 2.5%. Retailers like Target (down 11.4% on April 3) and Walmart (projecting $12 billion in costs) struggled, while others like Nucor gained 5%. The U.S. dollar appreciated 1.8% against the euro and 2.4% against the yuan within days, driven by expectations of a more insular economy. This strength, however, threatens U.S. exports—valued at $1.8 trillion in 2024—since a stronger dollar raises prices abroad. The soybean sector, which exported $28 billion last year, is already bracing for losses if China retaliates as it did in 2018, when its tariffs slashed U.S. soy exports by 74%. This aggressive stance reflects Trump’s belief that tariffs are a blunt but effective tool to force concessions, yet the scale risks alienating allies like Canada, potentially fracturing the USMCA. The China exemption for electronics suggests pragmatic concessions to consumer demand, but the 245% tariff signals unrelenting pressure on Beijing, which could backfire if retaliation escalates. The 90-day pause buys time but underscores the policy’s volatility, creating uncertainty for both markets and negotiators.

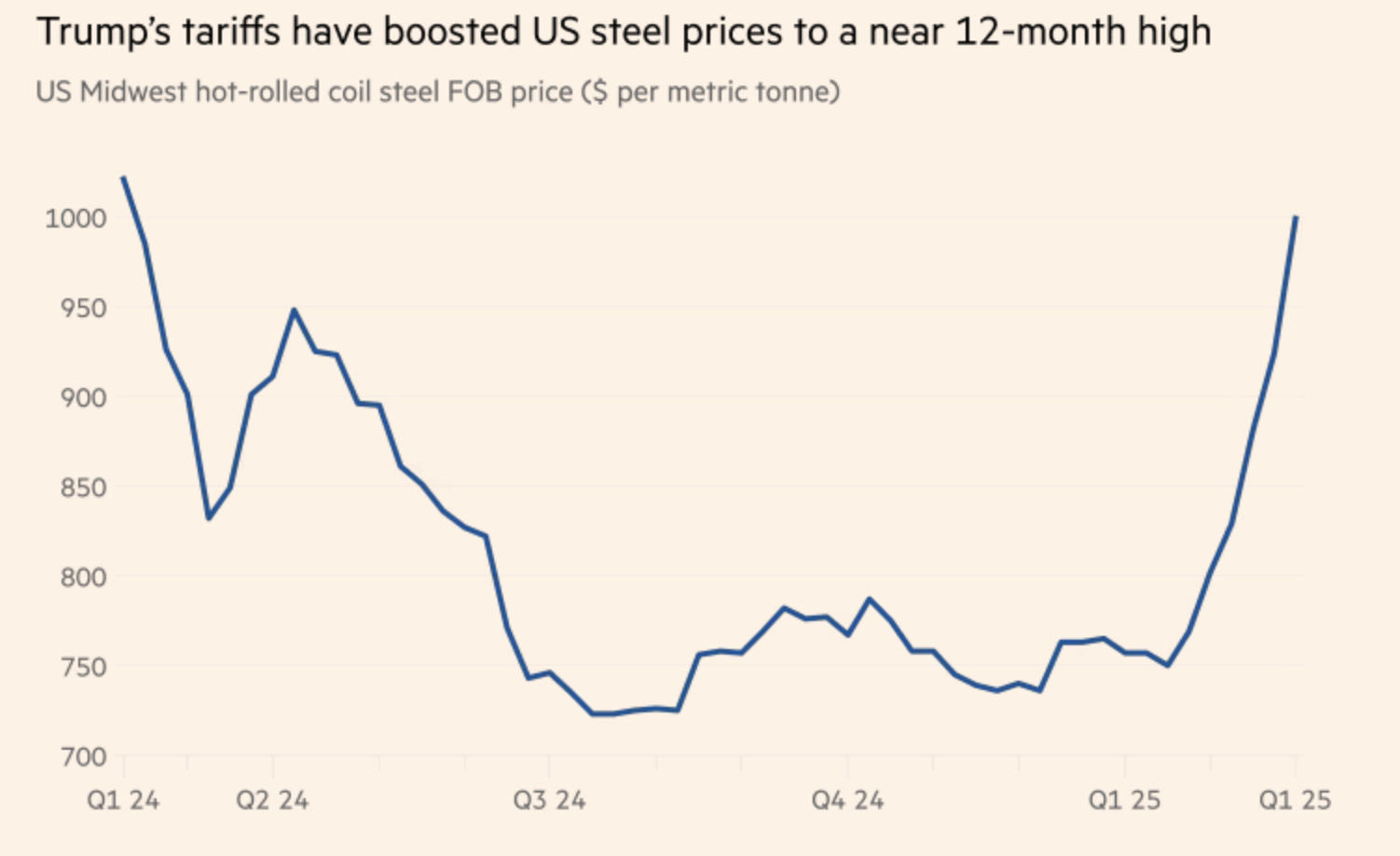

Winners and Losers in the Market

The latest round of tariffs has deepened the divide between winners and losers in the U.S. economy, sending ripples through markets and industries.

Winners: Domestic Producers and Small Manufacturers

U.S. steel and aluminum producers are among the biggest beneficiaries. Nucor and Steel Dynamics are well-positioned for gains as new tariffs—highlighted by a 245% duty on Chinese metals—are expected to add 6,000–8,000 jobs by 2027, building on the 3,200 steel jobs (a 4% increase) created after the first tariff wave.

Small manufacturers, employing over 2 million workers nationwide, are poised for revenue growth of 8–12% as import competition weakens. Sectors like machinery and chemicals stand to gain. The market is responding: the Russell 2000, tracking U.S.-focused companies, surged 8.7% on April 9, with Caterpillar shares up 4.3%.

Losers: Importers, Exporters, and Major Retailers

Import-heavy companies are taking a hit. Amazon, which sources 40% of its inventory from China, faces $10 billion in added costs—potentially shrinking profit margins by 2–3%. Walmart and Target project $18 billion and $5 billion in additional expenses, respectively. Target shares fell 13.2% on April 15.

Consumers will feel the weight. The Consumer Technology Association warns of $150–$200 price increases for smartphones and up to $300 for laptops. Overall, households may see annual costs rise to $1,500–$1,800—nearly double last year’s burden—driven by a 20% jump in prices for retail and tech goods. Exporters are also reeling from China’s 84% retaliatory tariffs. Farm losses could reach $20 billion, with soybean revenue dropping 55% (about $15 billion) and pork exports down $3 billion as China turns to Brazil. Corporate America is bracing for impact: Delta Air Lines withdrew its 2025 forecast, citing trade uncertainty, and its stock dropped 12%. Boeing faces a potential $4 billion hit to its Chinese order backlog. Tariffs may bring short-term wins for U.S. manufacturers and political gains in the Rust Belt states, but the broader economy is feeling the strain. Importers and exporters are absorbing heavy losses, while consumers face rising costs across essential goods. Corporate pullbacks and market volatility signal growing investor concern over a prolonged U.S.-China trade standoff. As tensions escalate, the risk of long-term supply chain disruptions and slowed global growth continues to rise.

Global Supply Chains Under Pressure

Trump’s tariffs, including the 25% levies on Canada and Mexico and the 10% baseline on all $3 trillion of U.S. imports, are straining global supply chains at a critical juncture, with trade volumes still down 9% from pre-COVID levels in 2020. The U.S.’s reliance on imports—$1.2 trillion from North America, $800 billion from Europe, and $600 billion from Asia in 2024—makes it vulnerable to disruptions, directly impacting everyday citizens. For instance, 70% of U.S. auto parts come from Mexico and Canada, and a $1.2 billion cost surge for Ford and GM threatens 300,000 jobs, while price hikes of $2,000 per vehicle hit consumers in states like Michigan. Apparel imports, with $90 billion annually (20% from Vietnam, 15% from the EU), face $20 billion in cost increases, driving 20–25% price rises for brands like Nike and H&M, adding $300 annually to family clothing budgets. The EU, facing $200 billion in U.S. exports under the 10% tariff, may retaliate with $50 billion in duties on American whiskey and autos, risking $5 billion in losses for Kentucky distillers and Detroit automakers. Vietnam, a key apparel and electronics supplier, has seen a 300% export surge since 2018 but lacks capacity to fully replace other sources, leaving retailers like Gap struggling with delayed shipments.

China’s role, while significant, is just one piece of the puzzle: the 245% U.S. tariff and China’s 84% retaliation threaten $2 billion in rare earth supplies critical for Tesla’s batteries and Lockheed Martin’s defense systems, while $50 billion in potential Chinese subsidies could flood global markets with cheap goods. More broadly, shipping costs have risen 15% since March, with port delays at Los Angeles and Rotterdam up 20%, signaling logistical gridlock. The EU’s $400 billion tech export market to the U.S., including semiconductors from ASML, faces $40 billion in added costs, potentially delaying $80 billion in U.S. tech sales. Mexico’s $50 billion in auto parts exports could shift to Brazil, which is already absorbing $3 billion in U.S. pork exports redirected from China. Reshoring efforts, despite the CHIPS Act’s $52 billion, are sluggish—only 10% of planned chip capacity is online, with U.S. factory builds costing $1–$2 billion and facing labor costs 10–15 times higher than in Asia.

The tariffs expose the U.S.’s import dependency, hitting everyday citizens with higher prices for essentials like cars, clothes, and tech, while global supply chains buckle under the strain. Allies like Canada and the EU may pivot to alternative markets, risking long-term trade fragmentation. The slow pace of reshoring and rising logistics costs signal a protracted transition, with consumers and small businesses bearing the immediate burden.

Long-Term Market Implications

Trump’s tariffs will reshape global trade dynamics over the long term, with significant implications for economic growth and stability. The 10% baseline tariff on $3 trillion in U.S. imports, combined with targeted levies like the 25% on Canada and Mexico, is projected to reduce U.S. GDP by 0.5% ($125 billion annually) by 2027, while real exports are expected to decline by 8% ($150 billion), as allies like the EU impose $60 billion in retaliatory duties on U.S. goods such as pharmaceuticals and machinery, and Canada shifts $20 billion in energy exports to Asia. The White House forecasts $250 billion in domestic investment and 500,000 manufacturing jobs by 2030, cutting the trade deficit to $650 billion—a 31% drop. However, historical precedent—2018 tariffs cost 75,000 downstream jobs for every 1,000 steel jobs saved—suggests a net loss of 200,000 jobs by 2027. A 10% tariff could boost U.S. manufacturing output by $150 billion annually (6%) by 2030, requiring $350 billion in capital for new factories in autos and electronics, but scaling the workforce to 19.5 million (from 11.3 million) demands $600 billion in training and infrastructure.

The EU’s $500 billion export market to the U.S., including $100 billion in autos from Germany, faces $50 billion in cost hikes, potentially slashing European growth by 0.3% ($200 billion). Canada and Mexico, under USMCA strain, may redirect $70 billion in trade to South America, boosting Brazil’s economy by 1% ($30 billion) but costing U.S. exporters $25 billion in market share. The 245% China tariff could drive $12 billion in U.S. rare earth mining by 2035, while the CHIPS Act’s $52 billion unlocks $200 billion in chipmaking, targeting 20% U.S. chip supply by 2028, saving $50 billion in imports. Risks are steep: inflation may rise to 4–5% through 2030, eroding $450 billion in household wealth, while Fed rates could hit 5–5.5%, adding $35 billion in debt costs. Retail margins may shrink 4–5% ($60 billion), with the S&P 500’s P/E ratio dropping from 22 to 18, cutting $3 trillion in market cap by 2030.

Global trade fragmentation could cost the world economy $1 trillion annually by 2030, with emerging markets like Vietnam and India gaining $100 billion in redirected trade but facing $30 billion in new U.S. tariffs. Small businesses in the U.S. and EU risk 25% failure rates by 2027, with 120,000 firms potentially closing due to cost pressures. Solar manufacturing in the U.S. could see $20 billion in investment, creating 10,000 jobs, but aerospace exports (e.g., Boeing) may lose $40 billion as global partners diversify. The tariffs’ global ripple effects threaten a broader economic slowdown, with U.S. export declines and inflation hitting consumers hardest. Allies’ retaliatory measures and trade shifts could erode U.S. market access, while domestic gains may take years to materialize, testing investor and political patience.

Investor Sentiment and Uncertainty

Investors are navigating a turbulent landscape as Trump’s tariffs disrupt global markets, with the 10% baseline tariff and 25% levies on Canada and Mexico amplifying uncertainty. The VIX spiked to 57.96 on April 7 and hit 40.1 after the 245% China tariff on April 15, far above last year’s average of 20, signaling heightened fear. Hedge funds have deployed $5 billion into battered sectors like autos and retail, betting on a rebound, while $8 billion has flowed into safe havens like utilities (up 3.8%) and healthcare (up 3.4%). The Nasdaq dropped 5.2% on April 16 as global supply chain fears hit tech giants like Nvidia, while the Russell 2000 held a 6.8% gain from April 9, buoyed by domestic firms like Deere & Co. (up 4%). Trading activity surged, with options volume up 30%, $2.5 billion in bearish bets, and $3 billion in tariff-hedged ETFs.

Trump’s policy swings have rattled markets: on April 7, he claimed tariffs would “make billions,” but after a market plunge, he paused most tariffs on April 9, only to escalate the China tariff to 245% on April 15, declaring, “We’re taking back control.” His April 15 Detroit speech promised $100 billion in tax breaks, deregulation, and $50 billion in infrastructure bonds, lifting steel stocks like Nucor 6.5% and energy firms like Occidental 3%, but broader indices faltered, with Fed rate cut odds rising to five in 2025. The EU’s potential $60 billion in retaliatory tariffs on U.S. autos and tech has investors shorting exporters like Ford, while Canada’s $20 billion trade shift to Asia threatens energy stocks like ExxonMobil. Emerging markets like India, gaining $40 billion in redirected tech exports, offer opportunities, but their $10 billion exposure to U.S. tariffs keeps investors cautious.

The 245% China tariff has heightened U.S.-China tensions, with China’s 84% retaliation threatening $50 billion in U.S. exports, but the broader global fallout—EU and Canadian retaliation, trade shifts to Brazil and India—dominates investor concerns. Markets crave stability, and Trump’s erratic approach—pausing tariffs one day, escalating the next—has Wall Street in a holding pattern, with global trade fragmentation and inflation risks overshadowing domestic gains. Investors are hedging aggressively, balancing opportunities in emerging markets with fears of a prolonged global slowdown. Inflation without delivering promised jobs, leaving Wall Street in a holding pattern as the U.S.-China clash intensifies.

Conclusion

Trump’s tariffs, with a 245% levy on China and a 10% baseline on $3 trillion in global imports, promise 500,000 U.S. jobs but threaten $1,800 in household costs, $150 billion in export losses, and a 0.5% GDP decline as of April 17, 2025. Markets remain unstable—the S&P 500’s 9.5% surge reversed with a 4.5% drop—while global supply chains strain under retaliatory pressures from the EU, Canada, and beyond. With trade fragmentation accelerating and inflation risks mounting, Trump’s strategy sets the stage for a high-stakes economic reset, challenging global markets to adapt to a new era of trade dynamics.

Thanks for reading my article!

If you’d like to see more content like this, check out more of my writing!